By Calum MacRae, Director, Supply Chain & Know-how,

S&P World wide Mobility

With power costs in Europe skyrocketing, positioning company

base strains in triage manner, a severe winter season could spot selected

automotive sectors at danger of being unable to maintain their creation

strains working.

The put together black swan occasions of the COVID-19 pandemic and the

Russian invasion of Ukraine have now stretched the automotive

provide line – specially in regard to semiconductors. Now, some

OEMs and suppliers with electrical power-intense producing processes

could confront intensive tension in terms of energy expenditures in the coming

months.

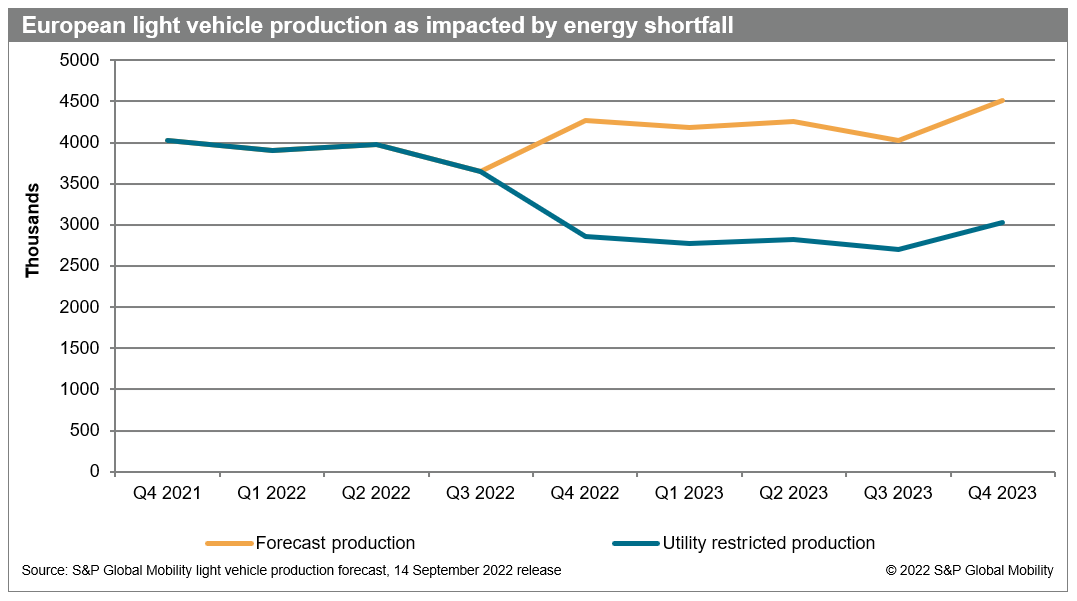

As a end result, likely manufacturing losses from Europe-based

OEM closing-assembly vegetation could reach extra than 1 million units for each

quarter, setting up in the fourth quarter of 2022 by the

entirety of 2023, in accordance to forecasts by S&P Global Mobility

and S&P Commodity Insights.

Setting up in the fourth quarter of 2022 as a result of 2023, quarterly

production from Europe-based mostly car producing crops was forecast

to be in the 4-4.5-million-device vary for each quarter – predicting

average advancement. Even so, with probable utility restrictions, that

OEM output could be minimized to as small as 2.75-3 million models per

quarter.

As viewed with past regional activities – Ukraine-sourced neon

shortages hampering semiconductor deliveries, and the 2011 Japan

earthquake and tsunami crippling provides for microcontrollers,

mass-airflow sensors, and Xirallic paint pigments – dropping just one

vital piece in the world-wide source chain can deliver the automotive

producing business to a crunching halt.

The consensus forecasts for a chilly, wet European La Niña wintertime,

merged with electricity shortages, could have a equivalent impact. The

current leaks in the subsea Russian pipelines to Europe adds to hazard

and the probability that our model is directionally accurate.

S&P World Mobility is forecasting important offer chain

disruption from November by way of spring. We also foresee

disruption of the conventional just-in-time provide model thanks to some

suppliers applying a plan of functioning fractional-months on a

24/7 setup – which can be more power-efficient than regular

weekly shifts thanks to the latter’s bigger start off-up and shut-down

electrical power fees.

We think about mandatory energy rationing to be the foundation for a

pessimistic situation for the region’s car producers and suppliers.

For an market now having difficulties with minimal inventories of vehicles

in seller showrooms, an extra disaster could be incapacitating

on a global scale.

European suppliers mail sections, elements, and modules to OEMs

all over the planet – thus impacting all automakers, not just regional

types. And U.S. retail customers could also undergo, as EU/British isles

production vegetation are at this time exporting about 7,000 models for each

month to American shores – but shipped 213,750 cars in the

entirety of 2019, in accordance to World-wide Trade Atlas.

“If you glimpse by means of the offer chain – specifically wherever

you can find any metallic framework forming via pressing, welding or

extrusion – you will find a huge amount of money of electrical power concerned,” mentioned

Edwin Pope, Principal Analyst, Elements & Lightweighting at

S&P World Mobility. “Whole electricity utilization in these corporations

could be up to just one-and-a-half instances what we are viewing in automobile

assembly these days. Anecdotally, we are listening to that some of this

production potential is getting so uneconomic that providers are

only shutting up shop.”

Right before the power crisis, gas and electrical expenditures were a

reasonably inconsequential element of a vehicle’s bill of

resources, ordinarily much less than €50 for every vehicle. Now with cost

increases ranging from €687 to €773 per vehicle, strength costs

compound an by now perilous placement for the sector – offered the

affect raw substance price raises have currently experienced on the nascent

electric powered vehicle value chains. Each serve to undermine margins in a

market where price increases will be challenging to pass on to

consumers currently struggling with food stuff and electricity inflation.

Across the European Union, electricity constraints could consequence in

nations or regions enacting crisis policies to counter this

risk. OEMs also have a specific amount of countervailing energy with

the regional utility firms and via governmental lobbying

functions.

“Nevertheless, the tension on the automotive offer chain will be

extreme, particularly the far more just one moves upstream from car or truck

production,” Pope said. “Upstream supplier areas creation

constraints could effects OEM volumes. As a consequence, we see a threat of

OEMs halting shipments of completed automobiles thanks to shortages of

single components, which are not essentially coupled to

state-stage energy procedures.”

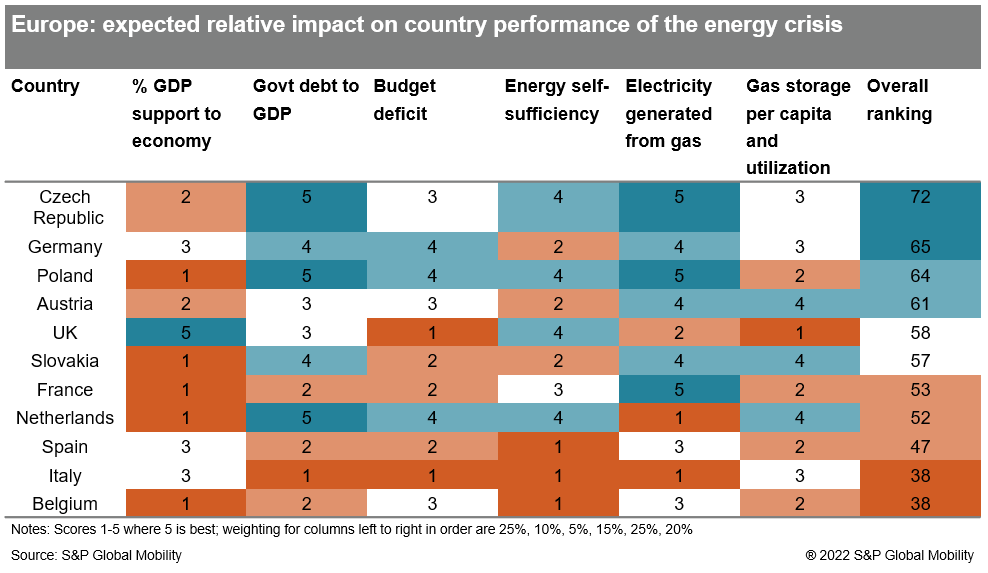

How nations will be able to react

S&P Global Mobility has modeled the impact of the looming

energy crunch on 11 European international locations – every a considerable motor vehicle

output location – to evaluate which countries’ automotive

segments are finest positioned to stand up to the severe electricity

headwinds this wintertime.

The product borrows from macroeconomic combination desire frameworks

in evaluating intake, financial investment, and government expenditure to

which an evaluation of electricity combine and gas storage is extra. Based

on a quantitative evaluation of available details, 6

proportions are scored on a relative basis among 1 and 5, with 5

getting the best rating.

The result the power disaster could have on a country’s financial

effectiveness and societal wellbeing can also be related to a

country’s industrial footprint. The most electricity intensive

industrial sectors are aviation and transport, but their power

consumption is tied practically solely to oil, where by value

improves have not been of the magnitude observed in fuel and

electrical power. Industrial sectors that see high utilization of fuel and

energy include things like chemicals and metallic goods, both equally of which

are intrinsically tied to automotive production.

Specific countries’ coverage responses in addressing vitality

imbalances will also impression comparative financial overall performance. These types of

insurance policies will determine how a country’s electricity blend impacts the

comparative advantage of car or truck establish places in Europe.

That affect is demonstrated by some counterintuitive outcomes in the

S&P World Mobility investigation. Germany has relied on Russia for

its fuel supplies and is phasing out nuclear electrical power, each of which

would feel to location that country in a precarious strength scenario.

Nonetheless, Germany added benefits from its government’s popular fiscal

rectitude, which provides it somewhat extra budgetary headroom to

ride out the electrical power storm. Further, the country positive aspects from a

fairly minimal reliance on electric power technology derived from gas

and from being in a decent situation from a fuel storage

standpoint.

The design also reveals how vital govt intervention in

residence and sector assist has been for the British isles. In the previous handful of

months, the British isles authorities has declared steps introducing up to some

GBP200 billion for shoppers and sector – accounting for approximately

7% of the country’s GDP and additional than double the stage of its

nearest rival Italy. With no these types of aid, the Uk would be around the

bottom of the table, in a place identical to that of Italy – which

suffers doubly owing to its credit card debt and finances deficit posture as

perfectly as its small electrical power self-sufficiency and reliance on gasoline electric power

for electrical power era.

The chart also delivers into concentration the relative placement of a

country’s macroeconomic placement vis-à-vis power and macroeconomic

insurance policies. Italy is a person of the far more susceptible economies, and this

weak spot will be even more compounded by the relative price tag

downside its manufacturing base faces.

Not all nations will be impacted equally by the energy industry

imbalances roiling marketplaces in Europe. That stated, it is very clear that

an period of plentiful, and low cost, electrical power is in excess of – and this has

stunned policymakers into varying levels of response.

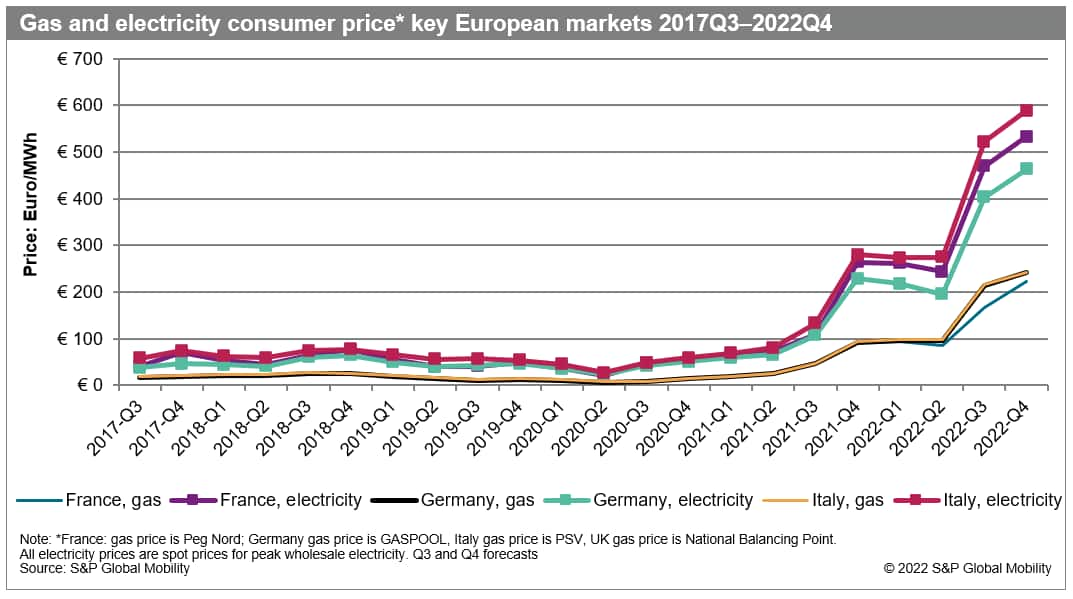

The impact of energy charges

Considering that very first quarter 2020, electrical power price ranges in Europe have soared.

According to S&P World-wide Mobility knowledge for four essential markets –

Italy, Germany, France and the British isles – fuel charges have enhanced by an

typical of 2,183%, a variable of almost 23. The wholesale energy

cost increased by an regular of 1,230% or a variable of more than

13.

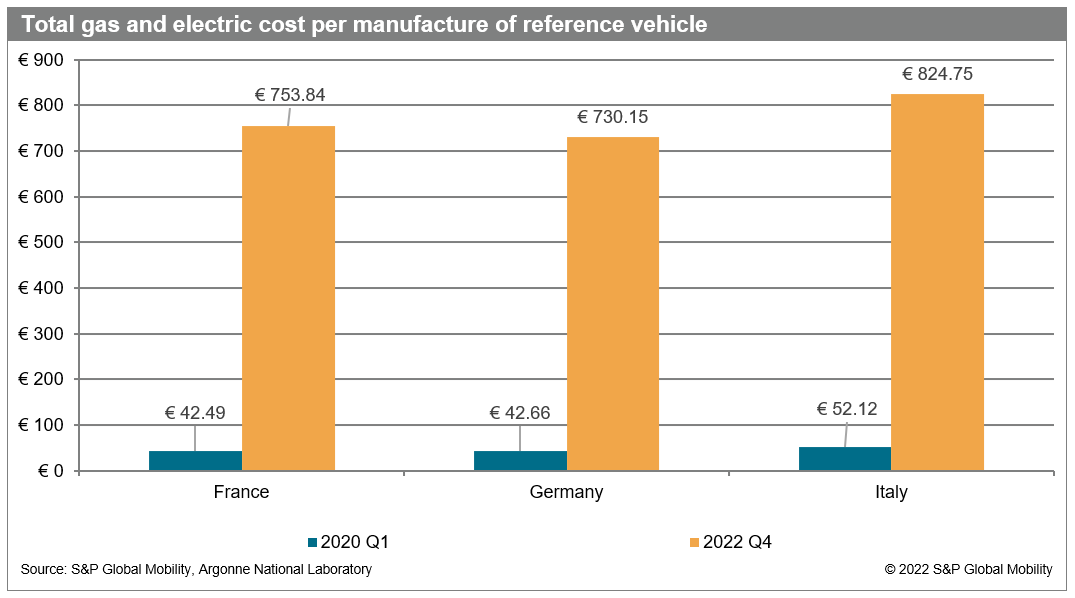

The effect of the surge in costs is proven starkly in the

subsequent chart. Making use of energy selling prices from the begin of 2020 and

evaluating with the present-day circumstance permits a check out of the

further charge that has been borne by OEMs. The subsequent chart

demonstrates the fuel and electric power price boost for a normal reference

auto across France, Germany, and Italy.

For superior-electricity intensity sectors like automotive manufacturing,

S&P International Mobility has created a methodology, leveraging

proprietary knowledge property, to estimate the effects on vehicle

manufacturing’s bottom line thanks to escalating vitality fees.

To permit for an apples-to-apples comparison in analyzing typical

electrical power utilization in each stage of final assembly, the solitary reference

automobile employed was a Volkswagen Golfing MKVIII, tipping the scales at a

shade less than 1,370 kg, and thinking about neighborhood vitality mix.

There are some caveats to this methodology. Carmakers from time to time

resource their vitality with distinctive mixes than the state the place

they work, whilst we presume similar strength sourcing in our

model. Automakers also tend to lock gasoline and electric power prices with

utilities and use various money instruments to cut down their

publicity – to the place they usually end up reporting important

windfalls from these hedging bets, as seen not long ago with the likes

of Volkswagen and Daimler. In our product, we assume they are spending

wholesale spot prices.

Ominous signs for the provider tiers

Irrespective of these warning signs, some OEMs protect their provider foundation

by indexing the rate of vital commodities monthly for their

suppliers, which indicates that some suppliers are not locked into

contracts at an inelastic price tag place by means of the length of the

deal. On the other hand, this practice is not completely widespread.

“As you go even more upstream, the sheltering the OEM offers

gets considerably less,” Pope claimed. “Also, scaled-down businesses in Tiers

2 and 3 of the provide chain are probable to neither have the

methods nor the operational sophistication necessary for hedging

devices, forward contracts and the like.”

The predicament Europe faces could be only transient. Considerably will

depend on how the Russia-Ukraine conflict unfolds. Nonetheless, a

for a longer time-phrase transformation of the vitality image could end result in

structural penalties for the market. This would see output

schedules, production footprints and sourcing approaches currently being

discarded and replaced with a change to places exactly where the vitality

value stress is minimum. When Europe faces a winter season of discontent

now, much more disruption could follow. This will provide elementary

upheaval to the region’s vehicle sector and further than.

In the way that labor charge made use of to be a important determinant of

manufacturing spot, electrical power blend and self-sufficiency could

become crucial features of long term sourcing decisions.

This posting was published by S&P World wide Mobility and not by S&P World-wide Ratings, which is a independently managed division of S&P International.

2024 Lexus LC 500 fixes its biggest problem with new touchscreen infotainment

2024 Lexus LC 500 fixes its biggest problem with new touchscreen infotainment  Chery Factory Tour – Double Apex

Chery Factory Tour – Double Apex  Just launched: Jeep Wagoneer / Hyundai Palisade / GAC Empow / Hongqi Ousado

Just launched: Jeep Wagoneer / Hyundai Palisade / GAC Empow / Hongqi Ousado  How To Get a Free Car From The Government 2023

How To Get a Free Car From The Government 2023  Great Wall Motors Reveals Ridiculous Six-Wheeler CyberP!ckup

Great Wall Motors Reveals Ridiculous Six-Wheeler CyberP!ckup  Auto Mechanics for Automotive Repair and Vehicle Repair in Abbotsford | FunRover

Auto Mechanics for Automotive Repair and Vehicle Repair in Abbotsford | FunRover  Smart budgeting strategies for tradespeople

Smart budgeting strategies for tradespeople  Exploring New Car Ratings: A Comprehensive Insight into Automotive Excellence

Exploring New Car Ratings: A Comprehensive Insight into Automotive Excellence  Vintage Ring Settings Loved by London Couples

Vintage Ring Settings Loved by London Couples