The most vital part of an car-bank loan is arguably the curiosity fee. It directly influences the dimension of every month payments and all round financial loan tenor. Curiosity rates can even play a part in the remaining getting selection, highly effective enough to override sentimental buy good reasons these kinds of as model loyalty. It goes without the need of declaring, therefore, that probable car prospective buyers pay out consideration to factors that identify their interest fees when procuring for auto-funding options.

One of these types of aspects is the credit score. It is effectively a weighted rating that tells automobile-loan providers how significantly chance they are having on by working with a prospective borrower. You most probable have a credit score report if you have any credit score accounts, this sort of as credit score cards, home loans or loans. This report then kinds the basis for analyzing your credit history rating.

It is not an specific evaluate, but it does shed gentle on elements this sort of as the borrower’s willingness and potential to services the bank loan. Merely set, the greater your credit score, the better your chances of securing an automobile personal loan with favourable desire costs. This is significantly crucial today as we navigate the period of interest rate hikes and inflationary pressures.

Working with your credit rating score to safe the greatest desire charges

By way of Experian

The over-all intent of the credit score score is common. Nevertheless, diverse lenders in diverse components of the earth have their individual standards to evaluate an individual’s creditworthiness. When you apply for an vehicle personal loan in the US, the financial institution will run a credit rating examine as aspect of the approach. The vast majority of the lending establishments use FICO credit scores. This is a 3-digit score assigned to a borrower just after the credit examine work out.

It was at first developed in 1989 by a details analytics company referred to as Reasonable Isaac Business. Right now, there are quite a few variations of the FICO algorithm (and other scoring types, for that make a difference), but they are all aimed at ascertaining the borrower’s skill to take on credit rating.

Via The Harmony

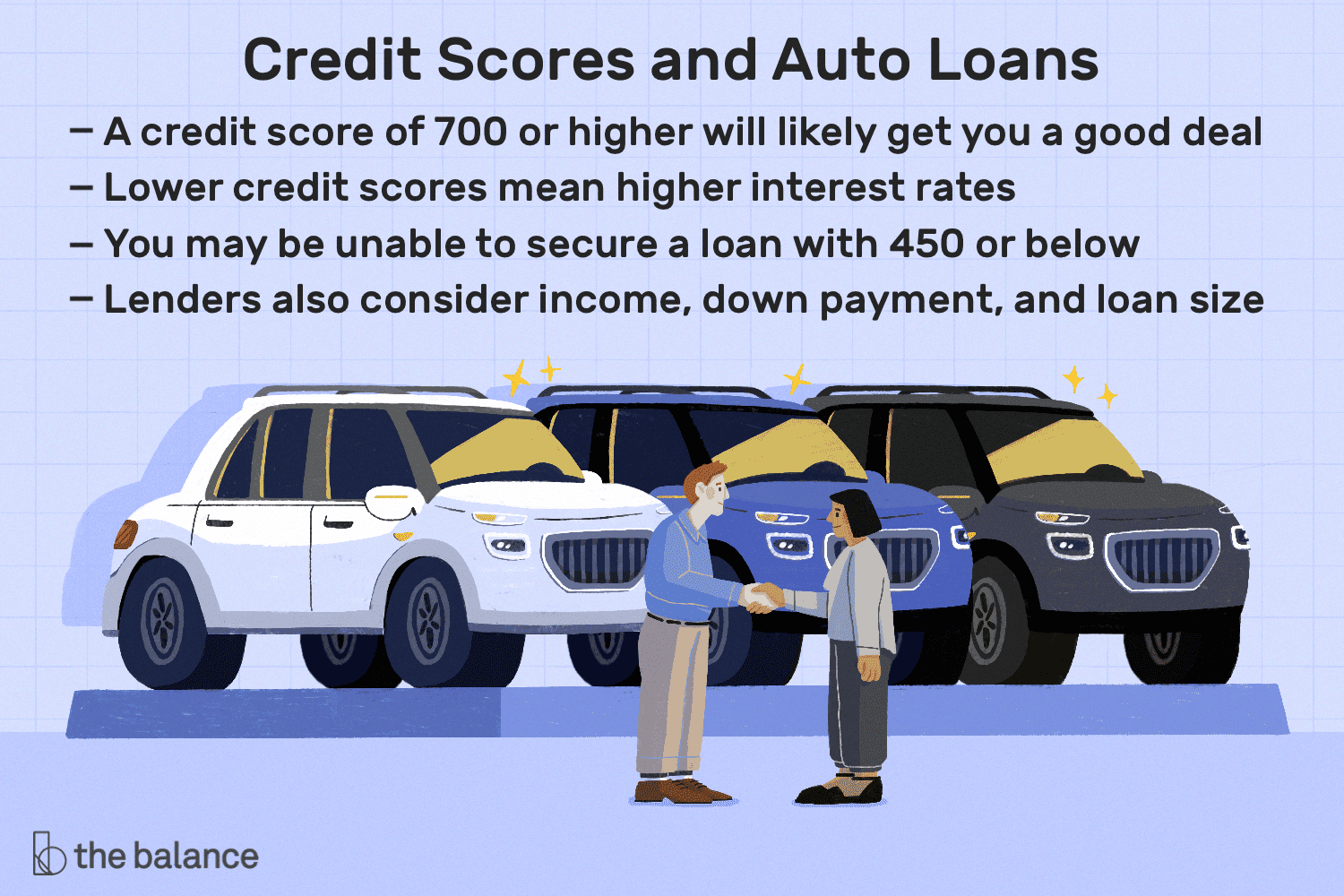

According to the CFPB (Client Monetary Defense Bureau) Purchaser Credit Panel, there are 5 various borrower profiles sorted into the following credit score score buckets: Tremendous-prime (720 & over) Prime (660-719) In the vicinity of-primary (620-659) Subprime (580-619) Deep subprime (underneath 580). A borrower with a rating below 660 can nonetheless protected automobile financial loans, but they will be extra highly-priced than a Prime or Super-prime borrower with a rating north of 661. The logic in this article is that you will want to preserve your credit score score as superior as achievable to get the most effective discounts when browsing for vehicle financial loans.

Issues that damage your credit score rating

Through Investopedia

An excellent credit score rating is the consequence of watchful and deliberate arranging, and figuring out the likely pitfalls can assistance the borrower prevent making missteps that pull down the rating into undesirable territory.

Earning a late payment

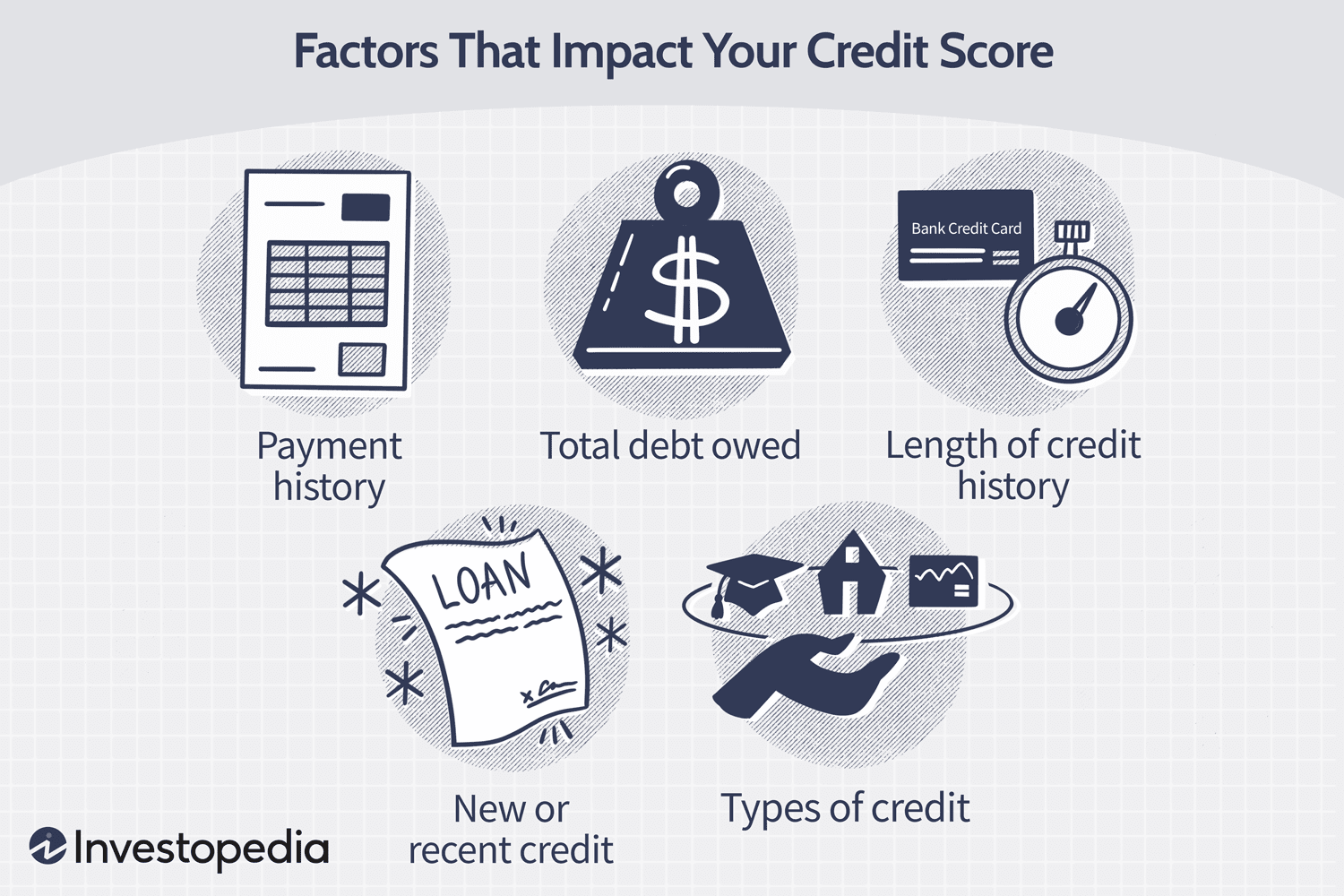

Payment history on your credit score obligations accounts for up to 35% of the FICO score. In accordance to FICO, a payment that is 30 days late can expense an individual with a credit score rating of 780 or higher any place from 90 to 110 details. It is critical to make payments as at when because of and proactively arrive at out to the loan provider if, for any reason, payment will be delayed.

A large debt-to-credit rating utilization ratio

Credit score history is designed by a continuous cycle of credit utilization and shell out downs. However, you will want to maintain an eye on the proportion of your credit card debt load to all round credit rating. The lessen your balances relative to your whole obtainable credit, the improved your score will be.

Non-utilization of credit score

On the other hand, no credit record for an prolonged period of time can also adversely impact the borrower’s credit history rating. Loan companies and lenders have absolutely nothing to report to credit score bureaus when you really do not benefit from your credit rating accounts. This tends to make it more complicated to consider potential mortgage programs.

Bankruptcy

Filing for individual bankruptcy has one particular of the most considerable impacts on your credit history rating. It can wipe as much as 240 details from an individual’s score, and what is a lot more? A bankruptcy report can keep on the credit rating heritage for up to 10 years.

This record is by no signifies exhaustive, and other things this sort of as frequency of credit history programs, credit history card closure, charge-offs and refinancing all influence credit rating scores in various levels.

Improving your credit rating score

Improving your credit score rating will involve staying away from the pitfalls previously recognized higher than. Procedures these types of as prompt and common monthly bill payments, maintaining a very low personal debt-to-credit score utilization ratio (ideally about 30%), maintaining credit rating card accounts open and averting quite a few mortgage programs at as soon as are all ways in the appropriate course.

Even so, even with all these ‘building blocks’ in place, a terrific credit score is not instantaneous. It may possibly acquire a whilst to see any advancement, specially due to the fact unfavorable stories can keep on your credit score history for numerous several years. There is no rigid time frame for credit rating expansion as every single person’s economical circumstance is exclusive. According to Forbes, it could consider everywhere from a month to as much as 10 yrs. Certainly, this is motivated by variables this sort of as the individual’s present credit history status and amount of money of whole exposure.

Securing automobile loans regardless of credit score score

Through Geotab

A substantial credit score rating will certainly increase your chances of securing automobile financing and locking up the most effective interest fees. On the other hand, it’s not all doom-and-gloom for potential automobile potential buyers with weak scores as they are not entirely with out options.

Regardless of your credit history score, on the lookout about and thinking of the various financing solutions is extremely advisable. It is just like procuring for the automobile alone an normal purchaser will appraise diverse dealerships and negotiate vigorously just before creating the ultimate final decision.

Banks are the standard resources for acquiring a loan, but you could be limiting your selections if they are your only thing to consider. Do not disregard substitute loan companies. Operating with 3rd-celebration financing providers, this sort of as acquiring your car financial loan by using LoanCenter.com, may possibly provide you with favourable curiosity charges or financing phrases.

It is important to observe that only getting car-mortgage preapprovals (various from precise financial loan applications) even though shopping about will not impression your credit rating score because most scoring products do not handle this as a challenging enquiry.

In summary, a weak credit history rating may perhaps push the cheapest fascination fees out of attain. However, having quite a few alternatives will strengthen your probabilities of discovering a deal with an fascination price that suits within your spending budget and allow you to invest in your sought after automobile.

Exploring New Car Ratings: A Comprehensive Insight into Automotive Excellence

Exploring New Car Ratings: A Comprehensive Insight into Automotive Excellence  The Ram 1500 Rebel Havoc edition is a bit of deja vu

The Ram 1500 Rebel Havoc edition is a bit of deja vu  F1 Live Updates: Miami 2023

F1 Live Updates: Miami 2023  Electric Corvette sparked on 70th anniversary

Electric Corvette sparked on 70th anniversary  Understanding and Bringing Uber Claims: Insurance and Your Rights

Understanding and Bringing Uber Claims: Insurance and Your Rights  Free Car For Unemployed From The Government 2023

Free Car For Unemployed From The Government 2023  Smart budgeting strategies for tradespeople

Smart budgeting strategies for tradespeople  Vintage Ring Settings Loved by London Couples

Vintage Ring Settings Loved by London Couples